Introduction

Building a house is a lifelong dream for many families in India. For most people, however, constructing a home requires a significant amount of money, which is not always possible to arrange at once. Because of this, many homeowners depend on a house construction loan to manage the expenses involved in building their dream home.

A house construction loan process in India helps finance the building work step by step, making it easier to complete your project without putting too much pressure on your savings. By understanding how the house construction loan process works in India, you can plan your finances better and avoid unnecessary delays during construction.

In this guide, we will explain the complete process of getting a house construction loan in India. You will also learn about the eligibility criteria, important documents needed for approval, interest rates, and how the loan is released at different stages of construction. This information can help you make better financial decisions and move one step closer to building your dream home.

What is a House Construction Loan?

A house construction loan is a specific type of home loan offered by banks and financial institutions to help individuals build a new house on their own land. Instead of buying a ready-built property, this loan is meant for people who want to construct their home according to their own design and requirements on a plot they already own.

Banks such as State Bank of India (SBI), HDFC Bank, ICICI Bank, Axis Bank, and LIC Housing Finance provide house construction loans with competitive interest rates.

A house construction loan process in India usually involves checking eligibility, submitting documents, getting plan approval, and receiving loan disbursement in stages during construction.

This loan helps individuals construct their dream house even if they do not have full funds available.

Eligibility Criteria for House Construction Loan

To apply for a house construction loan in India, you must meet certain eligibility conditions. These conditions may vary slightly depending on the bank, but basic requirements are similar.

Basic eligibility:

- Age between 21 and 60 years

- Indian citizen

- Salaried or self-employed with stable income

- Good CIBIL score (700 or above)

- Own plot with clear legal documents

- Approved house construction plan

Banks review your repayment ability and credit history before approving the loan. A higher income and a good credit score can increase your chances of getting the loan approved.

Documents Required for Construction Loan

Submitting the necessary documents is very important for quick loan approval. Missing or incorrect documents can delay the process.

Common documents required:

- Aadhaar card and PAN card

- Passport size photographs

- Salary slips (last 3–6 months)

- Income proof or ITR for self-employed

- Bank statements (last 6 months)

- Property documents of land

- Approved building plan

- Construction estimate by civil engineer

- Employment proof or business proof

Make sure all documents are genuine and updated to avoid rejection.

Factors Affecting Construction Loan Approval

Banks evaluate several factors before approving a house construction loan. Understanding these factors can improve your chances of getting the loan approved quickly.

Some important factors include:

• Credit Score – A credit score above 700 improves the chances of getting the loan approved

• Income Stability – Banks usually prefer borrowers who have a stable income and secure employment.

• Property Documents – The land on which the house is being built must have clear legal documents.

• Construction Plan Approval – The building plan must be approved by the local municipal authority.

• Loan Repayment Capacity – Banks review your existing loans and other financial commitments before approving the loan.

Maintaining a good credit profile and submitting the required documents can greatly improve your chances of getting a construction loan.

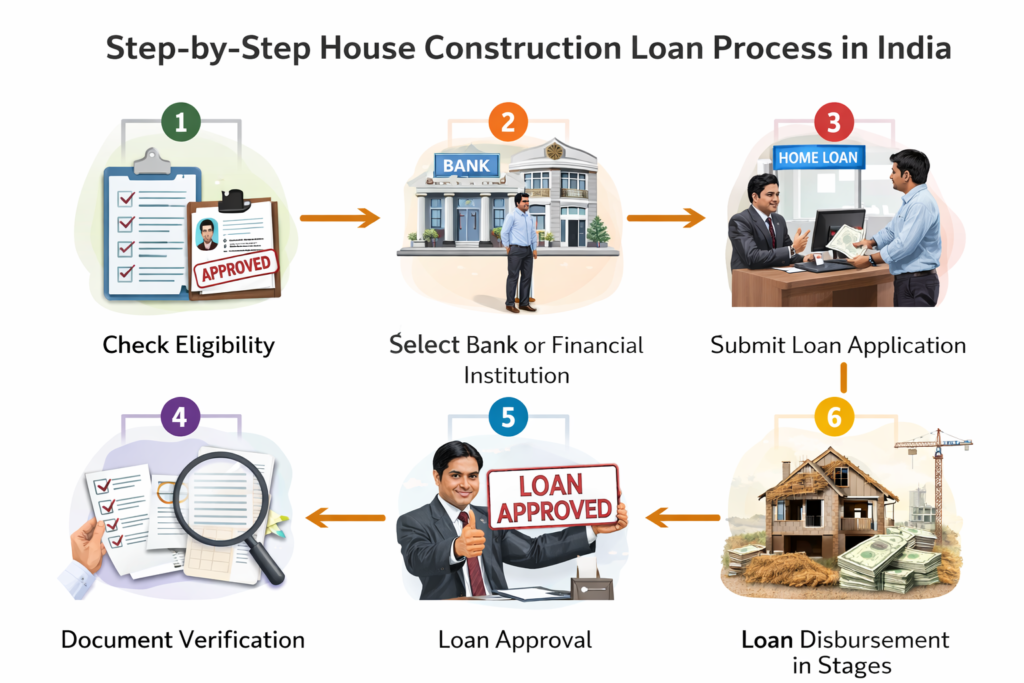

Step-by-Step House Construction Loan Process in India

Understanding the house construction loan process in India helps you apply easily and avoid confusion. Below is the step-by-step process.

Step 1: Check Eligibility

Before applying, check your eligibility based on income, age, and credit score. You can check eligibility online on bank websites.

Step 2: Select Bank or Financial Institution

Compare interest rates, processing fees, and repayment options of different banks. Choose a reliable bank that provides low interest rates and flexible EMI options.

Step 3: Submit Loan Application

Complete the loan application form and submit the necessary documents. You can apply online or visit the nearest bank branch.

Step 4: Document Verification

The bank will verify your income, property documents, and credit score. They may also conduct a site visit to check the plot and construction plan.

Step 5: Loan Approval

After successful verification, the bank approves the loan amount. You will receive a sanction letter that states the loan amount, interest rate, and repayment period.

Step 6: Loan Disbursement in Stages

Unlike home purchase loans, construction loans are released in stages:

- Foundation stage

- Basement or plinth level

- Roof level

- Finishing stage

The bank releases money after checking construction progress at each stage.

Construction Loan vs Home Loan – What is the Difference?

Many people often confuse a house construction loan with a regular home loan. However, these two loans serve different purposes.

A home loan is generally taken to buy a ready-built house or apartment. In contrast, a construction loan is specifically meant for building a new house on your own land.

In a construction loan, the bank releases the loan amount in stages according to the progress of the construction. For example, funds may be released during foundation work, roof slab construction, brickwork, and finishing stages.

Another key difference is that construction loans usually have a shorter repayment schedule during the construction period. Once the construction is completed, many banks convert the loan into a regular home loan.

Understanding this difference helps borrowers choose the right loan option according to their needs.

Loan Amount and Interest Rates in 2026

Banks usually provide 70% to 90% of the total construction cost as loan. The remaining amount must be arranged by the borrower.

Interest rate for house construction loans in 2026 ranges between:

8.5% to 10.5% per year

Interest rates depend on:

- Credit score

- Income

- Bank policies

- Loan amount

You can choose fixed or floating interest rate based on your preference.

Example of Construction Loan EMI Calculation

Let us understand a simple example of a construction loan.

Suppose a borrower takes a construction loan of ₹25,00,000 at an interest rate of 8.5% per year for 20 years.

Approximate EMI calculation:

Loan Amount = ₹25,00,000

Interest Rate = 8.5%

Loan Tenure = 20 years

The approximate EMI would be around ₹21,700 per month.

However, during the construction period, banks may charge pre-EMI, where you pay interest only on the amount disbursed.

Using an online EMI calculator can help you estimate monthly payments before applying for the loan.

Tips for Fast Loan ApprovalGovernment Schemes for House Construction Loan in India

The Government of India provides several housing schemes that help people build their own homes. One of the most popular housing schemes is the Pradhan Mantri Awas Yojana (PMAY).

Under PMAY, eligible homebuyers can receive interest subsidies on housing loans, which reduces the overall loan burden. This scheme is mainly designed to support economically weaker sections (EWS), low-income groups (LIG), and middle-income groups (MIG).

Borrowers applying for house construction loans can check whether they qualify for PMAY benefits. If eligible, they may receive interest subsidies under the Credit Linked Subsidy Scheme (CLSS).

These benefits can significantly reduce the effective cost of borrowing for building a house.

Advantages of House Construction Loan

There are several benefits of taking a house construction loan in India.

- Helps build your dream home without full savings

- Flexible repayment options

- Tax benefits under home loan rules

- Interest charged only on released amount

- Easy EMI payment options

- Long repayment tenure up to 20–30 years

A construction loan provides financial support and makes home building easier.

Benefits of Taking a House Construction Loan

Taking a house construction loan offers several advantages for individuals planning to build their own home.

Some major benefits include:

• Flexible Loan Disbursement – Banks release funds in stages based on construction progress.

• Lower Interest Rates – Construction loans often have competitive interest rates compared to personal loans.

• Tax Benefits – Borrowers may receive tax benefits on interest payments under certain conditions.

• Custom Home Construction – Borrowers can design and build a home according to their needs.

• Higher Loan Amounts – Banks may provide large loan amounts depending on income eligibility.

These benefits make construction loans a practical financing option for building a house.

Tips for Fast Loan Approval

If you want quick approval for your construction loan, follow these tips:

- Maintain CIBIL score above 700

- Submit genuine documents

- Provide accurate construction estimate

- Avoid existing loan defaults

- Choose reputed bank

- Maintain stable income proof

Proper planning and documentation increase approval chances and reduce delays.

You can also estimate your total construction cost using our Concrete Calculator before applying for a loan.

Common Mistakes to Avoid

Many people make mistakes while applying for construction loans. Avoid these common errors:

- Submitting incomplete documents

- Low credit score

- Choosing high-interest bank without comparison

- Wrong construction estimate

- Ignoring EMI repayment capacity

Avoiding these mistakes will help you get loan approval easily.

Before applying for a construction loan, it is also important to estimate the construction cost per square foot in India.

How to Choose the Best Bank for a Construction Loan

Choosing the right bank for a house construction loan is an important step in the borrowing process. Different banks offer different interest rates, processing fees, and loan terms. Comparing different banks helps you choose the most affordable loan option.

Before selecting a bank, it is important to check the interest rate offered for construction loans. Even a small difference in interest rate can significantly affect your total repayment amount over the loan tenure.

Borrowers should also compare processing fees, prepayment charges, and loan disbursement policies. Some banks release loan amounts faster during construction stages, which helps avoid delays in building work.

Another important factor is customer service and loan support. A bank that provides clear guidance during the loan process can make the construction loan experience much smoother.

Taking time to research and compare banks can help borrowers choose the best construction loan with suitable terms and lower financial burden.

Frequently Asked Questions (FAQs)

1) Can I get a construction loan without owning land?

No, most banks require the borrower to own the land before approving a construction loan. The land documents are necessary for legal verification.

2) How long does it take to approve a construction loan?

Construction loan approval usually takes 7 to 15 working days, depending on document verification and property approval.FAQ 1

3) Can I get a construction loan without owning land?

No, most banks require the borrower to own the land before approving a construction loan. The land documents are necessary for legal verification.

4) How long does it take to approve a construction loan?

Construction loan approval usually takes 7 to 15 working days, depending on document verification and property approval.

5) Which bank is best for a house construction loan in India?

Many banks in India provide house construction loans including SBI, HDFC Bank, ICICI Bank, and Axis Bank. The best bank depends on factors like interest rate, loan processing speed, and eligibility criteria. Borrowers should compare multiple banks before selecting the most suitable option.

For official housing loan guidelines and policies, you can also check the National Housing Bank (NHB) website.

Conclusion

Understanding the house construction loan process in India is essential for anyone planning to build a house. A construction loan provides financial support and allows you to build your dream home without paying the full amount at once.

Before applying, check your eligibility, maintain a good credit score, and prepare all required documents. Compare interest rates and choose the best bank for your needs. With proper planning and financial discipline, you can easily get a construction loan and complete your house without stress.

In summary, understanding the house construction loan process in India is essential for anyone planning to build a home. From checking eligibility and preparing documents to selecting the right bank and managing loan disbursement stages, each step plays an important role in the overall loan journey.

By maintaining a good credit score, submitting proper documents, and planning construction stages carefully, borrowers can improve their chances of getting a construction loan easily.

Before applying, it is always recommended to compare different banks, understand interest rates, and estimate construction costs to ensure a smooth and financially secure home-building process.

Shakeel T is a civil engineering enthusiast and founder of CivilGuide.in. He specializes in construction estimation, quantity surveying, and practical civil engineering calculations. Through CivilGuide, he shares real-world construction knowledge, calculators, and step-by-step guides to help students and site engineers improve their technical skills.